Cable One Deep Dive ($CABO)

Summary

I decided to take a look at Cable One (CABO 0.00%↑ ). They’ve typically had a higher multiple than the rest of the cable industry due to their unique footprint and less intense competition; however, the cable industry’s recent troubles have meant the valuation has come in (~9x EV/Ebitda from ~20x). The tl;dr version of this write-up:

A significant portion of CABO’s current customers will be overbuilt with fiber in the next few years. ~20% of CABO’s customers are from Boise/Gulfport; both these locations are in the process of fiber overbuilds (from AT&T & Lumen/CenturyLink). This increased competition and second viable broadband option will lead to pressure on both ARPU and customer churn.

Fixed wireless/5G is a significantly larger risk for CABO (than other cablecos) given their rural footprint. 5G operators are more focused on rural locations as they have significant excess spectrum to utilize. Additionally, CABO’s average broadband cost is >50% higher than some FWA options (~$80 vs ~$50).

At a ~7% free cash flow yield this is not cheap, and with the slowdown in an ever increasingly saturated broadband market, projecting significant subscriber growth appears optimistic. I’ll be passing on CABO.

Background

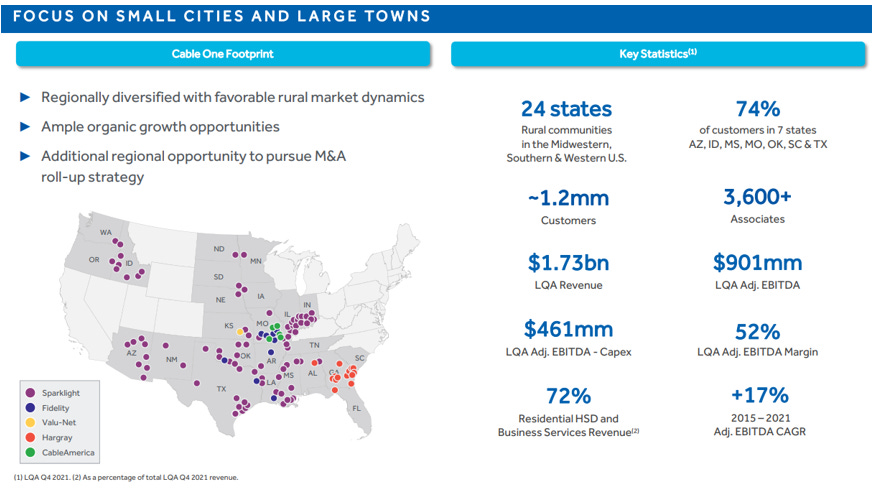

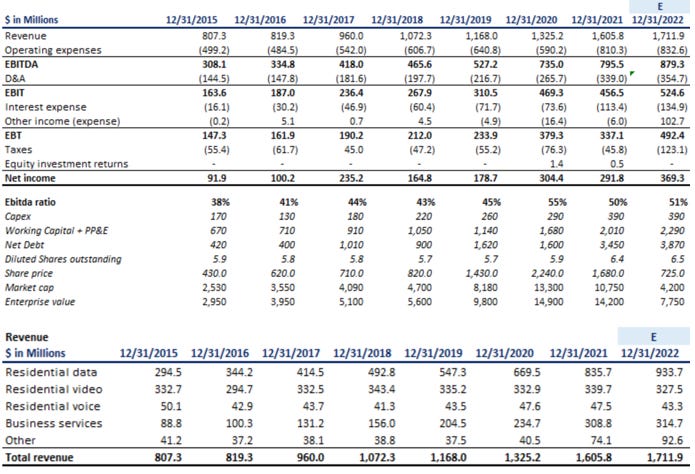

Cable One runs a data, video, and voice network that passes ~2.7mm homes/businesses and provides data services to ~1mm customers (38% penetration). They operate under the Sparklight brand, and their footprint is concentrated in 7 states (see slide from recent investor day below for some other general info).

Originally spun off in 2015 from Graham Holdings Company (GHC), Cable One (CABO) operates a unique business model that they believe differentiates them from other cablecos:

They focus on small cities and large towns (management call them safe harbor) where there is less competition; only ~1/3 of their footprint has a competitor that offers a wireline product >100mbps. They believe wireline competition will be slower to encroach on their footprint as the cost to build is high (less homes per square mile).

They deemphasized video early (~2013) and instead focus on providing internet as a standalone product with no long-term contracts; this has led to industry leading Ebitda margins (>50%). They use data caps to manage capacity on their network, and this tends push customers into higher plans and increases ARPU, ~$80 for CABO vs ~$65 for Charter/Comcast.

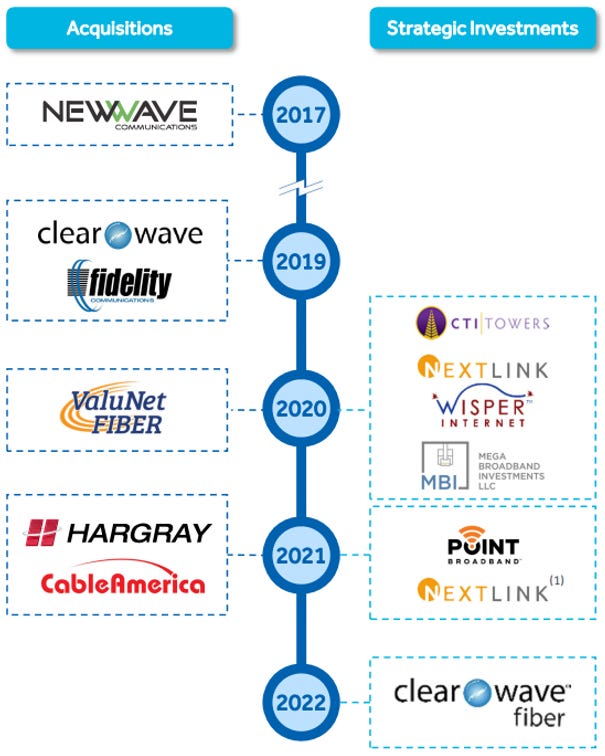

They are very active in the M&A market and focus on acquiring assets that follow a similar strategy to their own, mainly rural cable operators. They do also invest, to a smaller extent, in other types of technology such as fiber and fixed wireless. Given the large number of investments, I’ve detailed their activity over the last 5 years.

Acquisitions

CABO has made over 15 investments over the last 5 years; they’ve made full acquisitions, minority equity investments, formed joint ventures (JVs), and made investments with put/call options to purchase assets at a future date. I’ve detailed the investments below and put them in two buckets: key acquisitions/non-key (I’ve also added a slide below from a CABO’s investor presentation as a visual).

Key acquisitions

New Wave – May 2017

On May 1, 2017, CABO acquired 100% of NewWave for $740mm from GTCR (PE firm). This was CABO’s first large-scale acquisition and set the stage for further transactions with GTCR. The acquisition added ~430k passings and ~105k residential data customers in 7 states (IL, TX, LA, MO, MS, and AR). At the time of acquisition, NewWave was generating ~$180mm revenue and ~$65mm of Ebitda. NewWave is consolidated on CABO’s books.

Clearwave – Jan 2019 & Jan 2022

On January 8, 2019, CABO acquired Clearwave, a high-capacity fiber network that offered dense regional coverage in Southern Illinois. CABO paid ~$360mm on a debt free basis. The business passes ~20k businesses and has ~1.4k commercial customers (residential info not disclosed). The business generated ~$30mm annual revenue at the time of the acquisition. In January 2022, CABO contributed the Clearwave fiber assets to a JV (along with some of their Hargray fiber assets). The JV includes PE firm GTCR, and outside investors committed ~$320mm of capital to support expansion. The assets contributed passed ~74k homes and business and provided data services to ~14k customers. CABO owns 58% of the JV but the investment isn’t consolidated on CABO’s books, instead it’s reported as an equity method investment. The JV assets were ~3% of CABO’s revenue at the time of deconsolidation.

Fidelity – Oct 2019

On October 1, 2019, CABO acquired Fidelity Communications data, video, and voice related assets for ~$530mm (on a debt free basis). Fidelity had operations in 6 states (AR, IL, LA, MO, OK, and TX), with ~70% of customers in MO and OK. Fidelity passed ~190k locations and provided data services to ~72k homes (7k businesses). At the time of the acquisition Fidelity was generating ~$122mm revenue and ~$47mm of Ebitda. Fidelity is consolidated on CABO’s books.

MBI – Nov 2020

On November 12, 2020, CABO acquired a 45% (minority interest) in MBI for ~$575mm (from GTCR). MBI provides data, video, and voice services to residential and business customers in 16 rural markets (under the Vyve brand). MBI passes ~650k locations and provides data services to ~201k customers. LQA revenue at the time of the deal was ~$260mm. The investment is accounted for as an equity investment and is therefore not currently consolidated on CABO’s financials. In addition to the investment, CABO has an option to purchase the remaining equity in MBI between Jan 2023-June 2024. If this call option is not exercised, GTCR has the right to sell to CABO between July-Sept 2025. These options very likely mean CABO acquires MBI in the next few years and their results will eventually be consolidated on CABO’s financials.

Hargray transactions/acquisitions – Oct 20 & May 21

In Oct 2020, CABO contributed their Anniston system assets (~19k data customers in Alabama) to Hargray and in return received a 15% equity interest in Hargray. In May 2021, CABO acquired the remaining 85% of Hargray for ~$2bln ($2.2bln on cash and debt free basis). Hargray passes ~300k locations and had 108k residential customers (including the Anniston system CABO contributed), concentrated in the southeast. Hargray’s estimated annualized revenue was ~$295mm and Ebitda was ~$128mm at the time of acquisition. Hargray is consolidated on CABO’s books.

CableAmerica – Dec 21

On December 30, 2021, CABO closed on the acquisition of CableAmerica for ~$115mm ($95mm net of a $20mm tax benefit). The acquisition added ~53k residential passings (mainly in MO), generated ~$20mm in annualized revenue, and provided data services to ~13.5k customers (~1.25k business customers). CableAmerica is consolidated on CABO’s books.

Non-key acquisitions

May 20 – Acquired minority interest (<10%) in Nextlink for ~$27mm, a wireless internet service provider. In November 2021, CABO invested an additional $50mm to increase their ownership to ~17%. The investment is carried at fair value on the balance sheet and changes in fair value are recognized through the financial statement line item “Other income (expense)”.

July 20 – Acquired 100% of Valu-Net, a fiber service, for ~$39mm. The acquisition expands their footprint in Emporia Kansas and adds ~5k data customers. Valu-Net is consolidated in CABO’s financials.

July 20 – acquired a 40% minority interest in Wisper, a wireless internet service provider, for ~$25mm. Accounted for as an equity method investment (profit and loss flows through CABO’s income statement as a discrete line item “Equity method investment income”).

Oct 21 – Made a minority equity investment of ~$25mm for <10% of Point Broadband, a fiber internet service provider. This investment is accounted for in the same manner as Nextlink (see above). In March 22, CABO invested an additional $5.4mm to increase their equity interest to ~7%.

Oct 21 – Made a minority equity investment of ~$21mm for less <10% of Tristar, a special-purpose acquisition company (SPAC). This investment is accounted for in the same manner as Nextlink (see above).

Apr 22 – CABO contributed its Tallahassee Florida assets to MetroNet Systems, LLC, a fiber internet service provider in exchange for ~$7mm and a <10% equity interest. This investment is accounted for in the same manner as Nextlink (see above).

Jun 22 – Made a minority equity investment of ~$7.2mm for <10% of Visionary Communications, an internet service provider. This investment is accounted for in the same manner as Nextlink (see above).

Sept 22 - Agreed to Invest ~$50mm in Ziply, a fiber internet service provider, for <10% interest. CABO has funded ~50% of this commitment.

To summarize, CABO has invested ~$4.5bln in data related businesses since 2016; ~$3.6bln of these investments are consolidated on CABO’s financials. They’ve funded these acquisitions with cash on hand, debt (increased from ~$500mm to 3.8bln), and equity issuances (~$500mm).

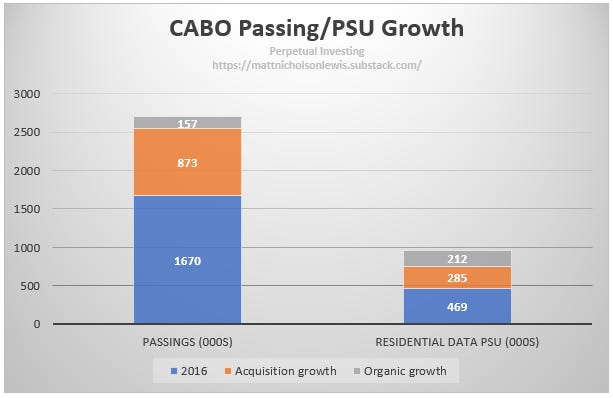

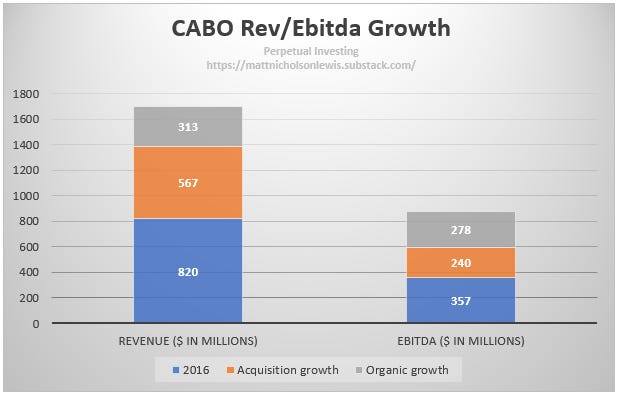

The below chart shows CABO’s estimated acquisition vs organic growth from 2016 through 2022 (please note all post acquisition growth has been accounted for as organic).

Hopefully the charts above will help put CABO’s growth in the correct context. They’ve been growing since the IPO, increasing data penetration from ~31% in 2016 to ~38% in 2022, as well as growing through acquisitions. Historical financial snapshot shown below:

This is a long introduction (sorry), but I think it’s necessary to understand CABO and their financials.

The Situation

Cable stocks have had a very difficult year due to multiple headwinds: Fiber and fixed wireless are both aggressively expanding their footprints, threatening cableco broadband monopolies, interest rates have risen dramatically in 2022, increasing the cost of capital, and the pandemic demand bump has faded, slowing broadband subscriber growth.

CABO hasn’t been immune to this pressure, and their stock is down ~60% ytd. They added only ~1k residential data subs in Q3 2022, vs 12k in Q3 21. They currently trade for ~9x EV/Ebitda, down from ~18x at the end of 2021. This write-up will focus on 3 questions that will be key to determining CABO’s fortunes as a business and stock over the next few years. I’ll also look at management before performing a rough valuation:

How much fiber overlap will there be and how will it impact CABO?

How will fixed wireless impact CABO’s rural business model?

What does broadband growth look like going forward?

Fiber

Fiber currently covers ~20% of CABO’s footprint and is expected to rise to ~35% by 2025, according to research from MoffettNathanson. The majority of this increase will come from CABO’s two main markets (Boise, ID and Gulfport, MS). These two areas make up ~225k of CABO’s data customers (~25% of their total).

Treasure Valley, ID - ~125k data customers. CABO’s biggest competition in this area (Boise) is CenturyLink/Lumen. Lumen has announced an overbuild of their copper footprint in this area and has started to light up their fiber network in certain locations. Before this overbuild, no competitor was providing broadband >100mbps. This can be confirmed by using highspeedinternet.com and searching Boise zip codes, or by using the new FCC broadband map.

Gulf Coast, MS - ~100k data customers. AT&T is CABO’s largest competitor here and is one of the metro areas AT&T has targeted (Biloxi-Gulfport) as they aim to pass 30mm homes and businesses with fiber by the end of 2025. There was some fiber in this area before AT&T’s new buildout, but not much (maybe covering ~20% of CABO’s Gulf Coast footprint).

{kind=link}

Outside of these markets, I don’t believe there’s significant fiber overbuilds planned in CABO markets. However, these overbuilds will mean new competition for up to 25% more of CABO’s current data customers. Competition will be new to CABO and how their model holds up is unknown. I have a few concerns.

As seen from other cablecos when fiber arrives, a subset of consumers switch to the fiber option very quickly. They might truly hate their current cable provider, or they might just want the better technology. CABO will have to deal with this like any other cableco experiencing a fiber overbuild, but their business model adds a couple of unique factors:

CABO’s data ARPU is ~$80, which is ~$10-15 higher than Charter/Comcast. This will make overbuilders more attractive as their promotional prices will be cheaper than CABO’s, and their post promotion prices will roughly match. Usually, in a cable/fiber duopoly, the fiber provider is slightly more expensive than the cableco; this won’t necessarily be the case in CABO’s markets and could open the door for higher terminal penetration for overbuilders.

Customers impacted by CABO’s data caps are going to be more likely to switch (CABO charges extra once you pass a certain usage threshold); cord cutting has also made bumping up against data caps more common. This will also give fiber a point they can push in local advertising.

This would concern me if I was on CABO’s management team. Your two largest markets have fiber coming over the next few years and using Charter/Comcast as a proxy for competitive dynamics is optimistic. High price points, data caps, as well as a less recognizable brand increase the risk of significant share losses.

Fixed wireless/5G

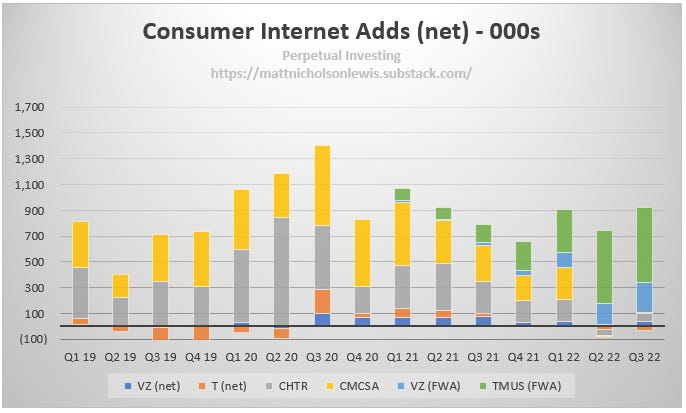

5G is the ultimate bear case for cable as it would turn competition in the broadband market from a duopoly with fiber, to a 5-way battle with wireless providers (AT&T, Verizon, and T-Mobile). This is especially worrying for CABO, as 5G is seen as a great way for wireless providers to utilize excess spectrum, predominantly in rural areas where CABO’s customers are concentrated. T-Mobile and Verizon’s fixed wireless offerings have taken most of the broadband ads in 2022, making this threat very real.

As I mentioned in my cable Q3 update, I think fixed wireless has increased the broadband TAM, rather than taking share directly from established cablecos. The biggest piece of evidence supporting this is Verizon’s FWA ads skewing heavily towards business customers (T-Mobile doesn’t disclose breakout so both consumer and business are included in their ads above); think construction sites that previously went without broadband as a wired connection wasn’t an option. Now they have access to broadband like speeds and all they need is a router placed on the site. My current belief is the likes of T-Mobile and Verizon are adding a significant number of connections that fit the scenario I just described. Additionally, they are converting legacy DSL customers who don’t have access to a high-quality cable or fiber providers (or customers with no wired connection option).

CABO’s business model, this time its focus on rural areas, means it is likely to be first in line when it comes to feeling 5G’s impact. While I believe that a wired option is still the best way to deliver internet, rural areas, where operators like T-Mobile have a significant amount of excess spectrum, increases the risk significantly for CABO. Again, their ARPU and data caps make them a target; T-Mobile’s offering of $50 for broadband, no data caps, and no contract seems like it was created to punish CABO for its business model (high ARPU and data caps). This situation will develop over the next few years as T-Mobile continues rolling out their fixed wireless offering neighborhood by neighborhood. The problem is, I’m not sure what CABO can do to stop this. T-Mobile can’t offer the same speeds/performance, but they offer a product that will be ~$300 cheaper (annually) and provides adequate speeds for the average household. CABO can offer promotions to customers that are considering switching or remove/change data caps, but either way there will be pressure on ARPU and churn.

Broadband market

The broadband market has been impacted by some macro factors over the past few years. The pandemic led to growth in broadband ads for the whole industry (see 2020 ad numbers above); now this tailwind has faded and cableco ads have slowed to nearly 0. Depending on who you ask though, you’ll get differing reasons for slowing growth.

The cableco explanation is lower move activity (Verizon subscribes to this as well). Move activity was ~12% lower in Q2 22 vs Q2 19, and cable companies like Charter, Comcast, and CABO claim they’re a share taker, so household movement is good for them. Cablecos claim they aren’t losing share to fiber, that 5G is an inferior product, and that current 5G ads are just future cableco ads (DSL —>FWA —> Cable).

Fixed wireless providers point to their ads and claim they’re taking share in areas where cablecos operate. Fiber overbuilders like Frontier tout share gains from cable as well, but their copper losses in most cases offset their fiber ads.

Like most things, the truth probably lies somewhere in the middle. On the cableco explanation, move activity likely explains some of the slowdown in their ads, but the main reason is the reversal of pandemic tailwinds. If you pull forward demand, by definition, it must be below trend after (it’s just math!). There are also customers who might be temporary broadband users, signed up out of necessity during the pandemic, or were taking advantage of government subsidies; CABO’s footprint likely means it has a higher amount of these potential “temporary users”.

Quick side note: on government subsidies, the benefit is still ~$30 a month under the ACP (down from ~$50 under EBB program) and >10mm households receive some type of benefit.

The fixed wireless explanation that they’re taking share in areas with a cable provider is a nice sound bite but comes apart pretty quickly when you dive a little deeper. ~85-90% of U.S. households are currently covered by cable, so of course ads are coming from an area with cable service… It doesn’t, however, appear they are currently switching, in a material way, customers signed up to established cablecos like Cable One, Charter, or Comcast. As mentioned above, Verizon’s make up of fixed wireless customers points towards an increased TAM, rather than converting cable customers.

My main concern for CABO is the pandemic tailwinds helped them more than others. CABO’s data penetration has increased from ~33% in 2019 to ~38% as of Q3 2022. Rural communities were more likely to go without internet pre-pandemic, and CABO was perfectly situated to take advantage of the increased need for connectivity as the country locked down. I wouldn’t be surprised if some of these newer customers are lower quality and are more likely to churn, especially when a fixed wireless offering that’s ~30% cheaper becomes widely available.

Management

Cable One has a very seasoned and long tenured executive team. Current CEO Julia Laulis has been with Cable One since 1999 and was named COO in 2012, before becoming CEO in 2015.

They’ve executed well on their strategy of rolling up small rural cable operators, increasing network performance, ARPU, and penetration. They successfully rebranded their offering to Sparklight in 2019 and have proven they can operate a profitable cable network with industry leading margins. Their Lead Independent Director, Tom Gayner, CO-CEO of Markel, is a widely respected investor and adds significant credibility to the board. Mr. Gayner recently increased his stake in CABO by ~80%, purchasing ~10k shares for ~$6.6mm (~$660 per share).

Management has, however, slipped up at times over the last couple of years. Hindsight is admittedly 20/20 but I personally think they got trigger happy with investments and they overpaid for some assets. The MBI deal in particular looks expensive. The original investment was at an implied valuation of ~$1.25bln for ~200k data customers. The call/put option structure likely means that CABO will end up owning MBI by 2025 (if the option price is below intrinsic value CABO will buy in their call option window and if the option price is higher, GTCR will sell at the option price). There’s not much information available on the strike price but the price to purchase the remaining 55% is “at a predetermined multiple of earnings”. Management has hinted they won’t be exercising the option early, and just using the carrying value of the put/call option on CABO’s books (~$35mm liability), as well as CABO’s multiple as a proxy (currently ~$9x, down from ~20x at the time of the deal), the put option owned by GTCR appears more valuable.

They’ve also levered the business significantly over the past 5 years to fund their acquisition spree, increasing debt from ~$500mm in 2016 to ~$3.8bln as of today. They have recently instituted a buyback, ~$300mm through Q3 of this year, but their increasing leverage will stop them getting more aggressive (~4x debt/Ebitda ratio).

My bias is against acquisitions (mainly as the stats say most don’t work out), but there’s no denying the success of CABO’s early acquisitions (NewWave, Fidelity etc.). They acquired strategic assets, improved network performance, data penetration, and Ebitda margins since gaining control. In the last couple of years however, I think they got a bit too aggressive with investments and overpaid (MBI, Hargray etc.).

Valuation

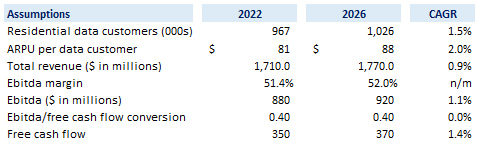

I usually make the point, at the start of any valuation, that the work is imprecise; I like to show a valuation in these write-ups though, as I think playing around with the numbers increases my understanding of the business and helps think through a reasonable base case. Additionally, I think it’s useful when you see analysis quantified in some way, even if it is very rough. The reason for this preamble is the key to pretty much any valuation is the multiple at the on the end of the forecast period. When you have a company like CABO, where the multiple has moved from ~20x to <10x in under a year, the roughness of the valuation must be emphasized even more than usual! With that out the way I’ve laid out key base case assumptions below:

Please note this base case assumes no acquisitions (even MBI which they will likely own by 2026 - MBI option valued at $0), an annual buyback of ~$200mm at $750 per share, and stock comp is accounted for by diluting share count 1% annually.

Broadbands ad growth stays sluggish over the next few years and CABO ads ~60k data customers. ARPU increases at a CAGR of ~2% to ~$88. Total revenue growth is ~1% as data revenue growth of ~5% is offset by high single digit declines in video and voice. Ebitda margins increase slightly as low margin video continues to become a smaller part of CABO’s business, as well as the successful integration of Hargray, offset by slightly higher cost of operations from DOCSIS 4.0 rollout and building some FTTH. Ebitda to free cash flow conversion stays consistent at ~40%.

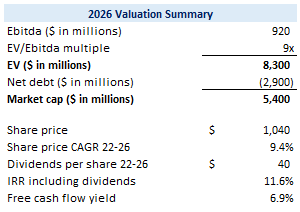

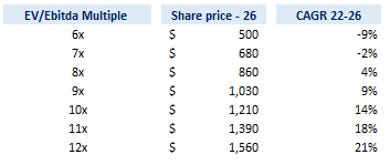

Looking out to 2026, we have a business generating ~$925mm of Ebitda and ~$370mm of free cash flow. I’m using a 9x multiple but have a sensitivity below to show impact of changing the multiple. I’ve also reduced net debt by ~$500mm to account for the value of the CABO’s unconsolidated investments (applying a ~50% haircut to be conservative). This gets us ~$1k a share in 2026 and a ~9% CAGR over the forecast period (~12% with dividends).

We’re taking on a significant amount of risk for this return though. The bull case is faster than expected broadband growth, slightly higher margins, and some multiple expansion; Maybe ~20% IRR?

The bear case is CABO starts to lose customers in Boise/Gulfport as fiber moves in (~20% of data customers). 5G becomes widely available and the price differential encourages customers to switch to fixed wireless. CABO starts bleeding subs across their whole footprint and the valuation multiple compresses further. Given the leverage, this leads to significant losses for the equity (maybe ~50%). For these reasons, I’m passing on CABO. In my opinion, Charter is a better choice if you’re looking for exposure to the cable industry (I’m long CHTR 0.00%↑ ). Thanks for reading.